An exceptional feed year, the grass is thick and a couple of weeks from ripening and turning brown as we prepare to wean our calves for market. It’s been our custom to cut firebreaks with the skid steer between our feed and Dry Creek Road. Last year we had eight arson sets that we were able to minimize with our 500 gallon water wagon. Fortunately, CalFire was able to identify and arrest the arsonists who are now in jail.

Despite our efforts and equipment, the ranch gets no discount for fire insurance premiums. Since PG&E was found culpable for the Northern California fires several years ago, we have found ourselves within the recently mapped High Risk Fire Area in California, and most all our neighbors have been dropped by insurance carriers. It seems apparent that PG&E’s losses and premiums have been spread out over the state. We are now investigating self-insurance for our home.

As a matter of business, insurance companies insure one another for catastrophic losses, and taken to the extreme, may in fact be one insurance company. Last year our insurance costs were 10% of our expenses, but unlike our other tangible expenses like hay and labor, we get only a little peace of mind in return at twice the price, if available.

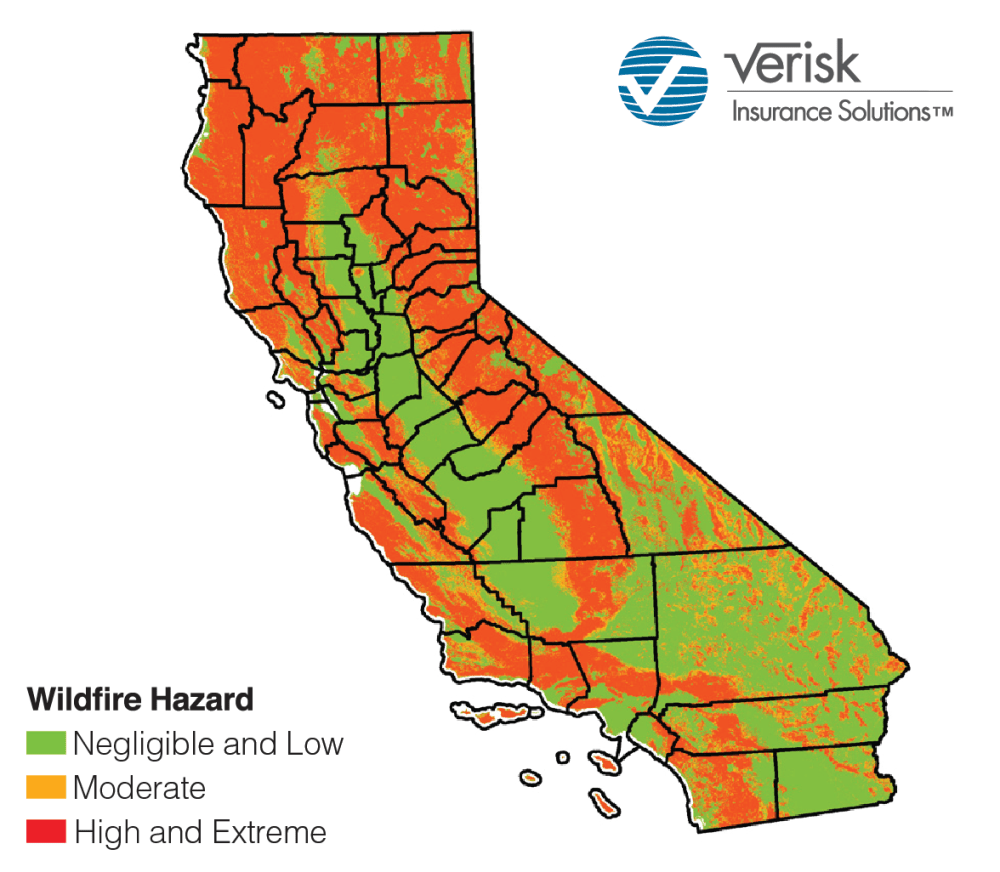

We are among the many home and ranch owners whose insurance policies have been canceled because they were located in the revised California’s High Risk Fire Area that includes almost half of the state.

Drought conditions in 2017, 2018, 2020 and 2021 combined with poorly maintained PGE transmission lines in Northern California charred over 8 million acres that left insurance companies holding the bag for losses and fire suppression costs. After a month-long process, we found one other carrier with less coverage at twice the cost.

A decade or so ago, Tulare County used to spray the weeds on the shoulders of Dry Creek Road to reduce fire danger from catalytic converters, hot brakes and dragging safety chains. Currently, 4-foot tall dry weeds encroach on the eroding asphalt adding to our risk of fire.

An independent onsite inspection was necessary to establish baseline conditions for home, barns, tack room and shop. I waited at the end of the driveway for the inspector from the Bay Area who had become lost. Up the drive in a cloud of dust she parked in the shade of a redbud as I followed in the Kubota. As she stepped out of her 2017 Chevy Volt, it began to roll down the slope, as she grabbed the door trying both to hold it and to get back in, towards our 500 gallon fire-fighting water wagon to veer at the last moment into the skid steer. She could have been seriously injured.

Though the hybrid rocked the skid steer upon impact, it survived unscathed. After assessing the damages to her car, we tied the plastic together with duct tape and hay string and tested the brake and turn signal lights. Drivable and legal, she went about her business of asking questions and photographing the structures while I showed her our firebreaks, plumbing for filling fire trucks and water wagon from our wells, while explaining that I had even stopped one fire myself with the skid steer.

Having made it home safely, she conducted the remainder of her inspection with questions over the phone and texts over the next two days. I repeated many of the photographs she had taken because of the glare from her cell phone, plus additional pictures of electrical service boxes and their manufacturers with interiors of all structures. In order not to have to dedicate another afternoon for another inspection, I essentially accomplished the onsite portion of her inspection.

I recount this calamitous and ill-advised process from a 75 year-old’s perspective, dumbfounded by the inefficient technological progress in that span of years. Frankly, she had no more business navigating and assessing rural California than we would be navigating and judging San Francisco, the ironic culture clash between us resounding loudly.